Introduction

When a life insurance policy is no longer needed or premiums become burdensome, policyholders often ask:

- Should I surrender my life insurance policy?

- Is a life settlement better than surrender?

- What is the difference between cash surrender value and a life settlement payout?

- Which option provides more value?

These are decision-stage questions. Understanding the structural differences between surrendering a policy and pursuing a life settlement is critical before taking action.

If you are unfamiliar with the broader concept, begin here:

Read More: How It Works & Policy Options

This article compares surrender and life settlement options objectively — including payout structure, eligibility, risks, tax implications, and regulatory oversight. This content is for educational purposes only and does not constitute legal, tax, or financial advice.

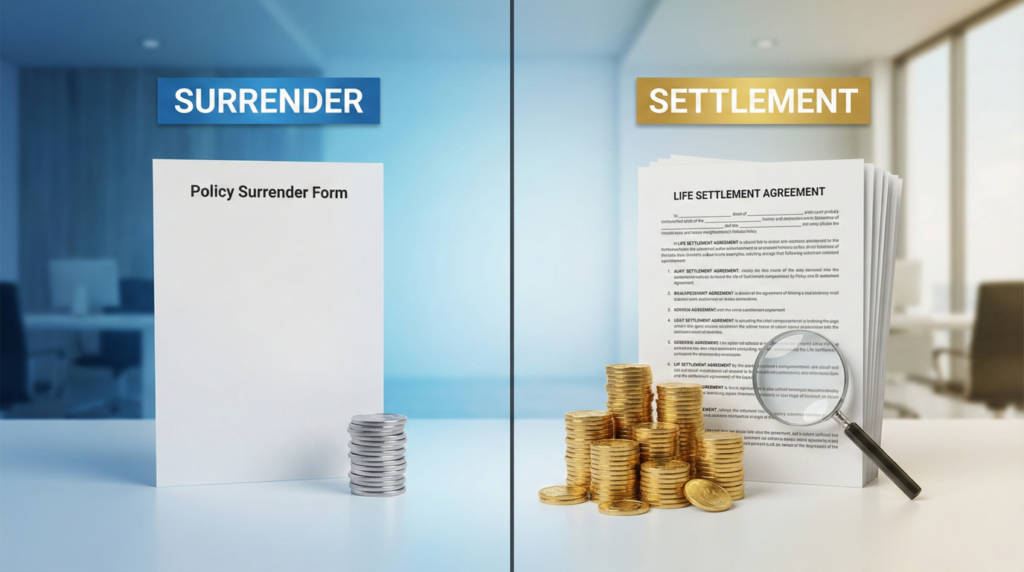

Quick Comparison: Surrender vs. Life Settlement

| Feature | Policy Surrender | Life Settlement |

|---|---|---|

| Who receives payment? | Policyholder | Policyholder |

| Payment amount | Cash surrender value set by insurer | Market-based lump sum offer |

| Typical payout range | Lower | Often higher than surrender value |

| Buyer involved? | No | Licensed third-party buyer |

| Death benefit retained? | No | No |

| Future premiums required? | No | No (buyer assumes) |

| Regulation | Insurance company rules | State-regulated transaction |

This table summarizes structural differences. Details matter.

What Is Policy Surrender?

Policy surrender means voluntarily terminating the life insurance policy directly with the issuing insurance company. In return, the insurer pays the policy’s cash surrender value.

The cash surrender value is:

- Determined by the insurance carrier

- Based on accumulated cash value (if permanent policy)

- Reduced by surrender charges (if applicable)

Once surrendered:

- Coverage ends

- Beneficiaries receive nothing

- The policy cannot be reinstated in most cases

Surrender is administrative and does not involve external buyers.

What Is a Life Settlement?

A life settlement is a regulated financial transaction in which a policyholder sells the policy to a licensed third party for a lump-sum payment.

The payment is typically:

- Greater than the policy’s cash surrender value

- Less than the full death benefit

After completion, the buyer becomes the new owner and beneficiary, and assumes future premium payments.

Read More: How the Life Settlement Process Works

Which Option Pays More: Surrender or Life Settlement?

This is the most common question. In many cases, life settlements provide more than the cash surrender value — but this is not guaranteed.

Why?

Because surrender value is determined internally by the insurance carrier. Life settlement value is determined through actuarial life expectancy modeling, discounted cash flow analysis, premium load forecasting, and risk-adjusted return modeling.

Read More: Who Qualifies for a Life Settlement?

If a policy does not qualify for a life settlement, surrender may be the only option besides lapse or reduction.

What Are the Tax Differences Between Surrender and Life Settlement?

Tax treatment varies. In general:

- Surrender proceeds may be taxable to the extent they exceed cost basis (premiums paid).

- Life settlement proceeds may have layered tax treatment depending on gain structure.

The IRS addressed certain aspects of life settlement taxation in Revenue Ruling 2009-13. You can read the official IRS PDF here.

Tax outcomes depend on cost basis, total payout amount, policy type, and individual tax profile. Consult a qualified tax professional before making a decision.

Read More: How Are Life Settlements Taxed?

What Happens to the Death Benefit?

In both surrender and life settlement scenarios, the original beneficiaries no longer receive the death benefit. This is often the most significant consideration.

The difference is:

- With surrender, the policy terminates entirely.

- With a life settlement, the policy remains active under new ownership.

Policyholders should evaluate estate planning implications before proceeding.

Read More: Risks of Selling a Life Insurance Policy

Are Life Settlements Regulated Differently Than Surrenders?

Yes.

Policy surrender is governed by the contract terms between the policyholder and the insurance company.

Life settlements are regulated primarily at the state level. Most states require licensed brokers/providers, disclosure forms, compensation transparency, defined rescission periods, and privacy protections.

The National Association of Insurance Commissioners (NAIC) developed the Life Settlements Model Act to standardize protections. Additionally, the U.S. Government Accountability Office (GAO) confirms state-level regulatory oversight.

Surrender does not involve a secondary market transaction. Life settlement does.

When Might Surrender Make More Sense?

Surrender may be appropriate when:

- The policy does not qualify for life settlement

- Cash value is minimal

- Premium burden is low and no better option exists

- The policyholder prefers administrative simplicity

- Estate planning needs are resolved

When Might a Life Settlement Be Explored?

A life settlement may be explored when:

- The insured is typically age 65+

- Premiums are burdensome

- Estate strategy has changed

- The policy has substantial face value

- There may be economic value beyond surrender

Qualification must be determined through underwriting.

Frequently Asked Questions (FAQ)

1. Is surrendering a life insurance policy the same as selling it?

No. Surrender means terminating the policy directly with the insurer. Selling through a life settlement transfers ownership to a licensed third party.

2. Does a life settlement always pay more than surrender?

Not always. Many life settlements exceed surrender value, but qualification and underwriting determine economic viability.

3. Can I compare surrender value and life settlement offers?

Yes. Policyholders may request surrender value from the insurer and evaluate whether a life settlement review is appropriate.

4. Is surrender faster than a life settlement?

Yes. Surrender is typically administrative and faster. Life settlements require underwriting and regulatory documentation, which may take several weeks.

For more answers, check out our FAQ page.

Key Takeaways

Surrender:

- Administrative

- Carrier-determined payout

- Immediate termination

- No third-party involvement

Life Settlement:

- Market-based valuation

- Regulated transaction

- Underwriting required

- Buyer assumes premiums

Neither option is inherently superior. The appropriate path depends on eligibility, financial planning objectives, tax considerations, and estate strategy. Before making a final decision, it may be prudent to understand both options fully.

Read More: How the Life Settlement Process Works

Want to see if a life settlement offers more value than surrender? Start an Educational Review with us today.