The recurring question. A long-funded Irrevocable Life Insurance Trust holds a policy whose original planning purpose — estate liquidity, equalization, business continuity — has shifted, expired, or become impractical to sustain. The trustee is left with a fiduciary decision: keep the policy, distribute it, sell it, or surrender it. Each path carries different consequences for the trust, the beneficiaries, the grantor, and the tax posture of the eventual proceeds. This guide walks through the framework practitioners should apply when an ILIT-held policy reaches that decision point, with attention to Crummey-power mechanics, the transfer-for-value rule, and the practical documentation a trustee needs.

The trustee’s baseline duty

The Uniform Prudent Investor Act, adopted in some form by nearly every state, requires a trustee to manage trust property as a prudent investor would. When the trust property is a life insurance policy, that duty implies an ongoing review of whether the policy continues to serve the trust’s purposes — and, where it does not, whether continued payment of premiums represents a prudent use of trust resources or beneficiary contributions.

A passive trustee who simply pays premiums year after year without periodic review risks a fiduciary claim from beneficiaries who later discover that a settlement or other disposition would have produced materially better trust outcomes. Periodic policy review — ideally annually — is the baseline practice expectation.

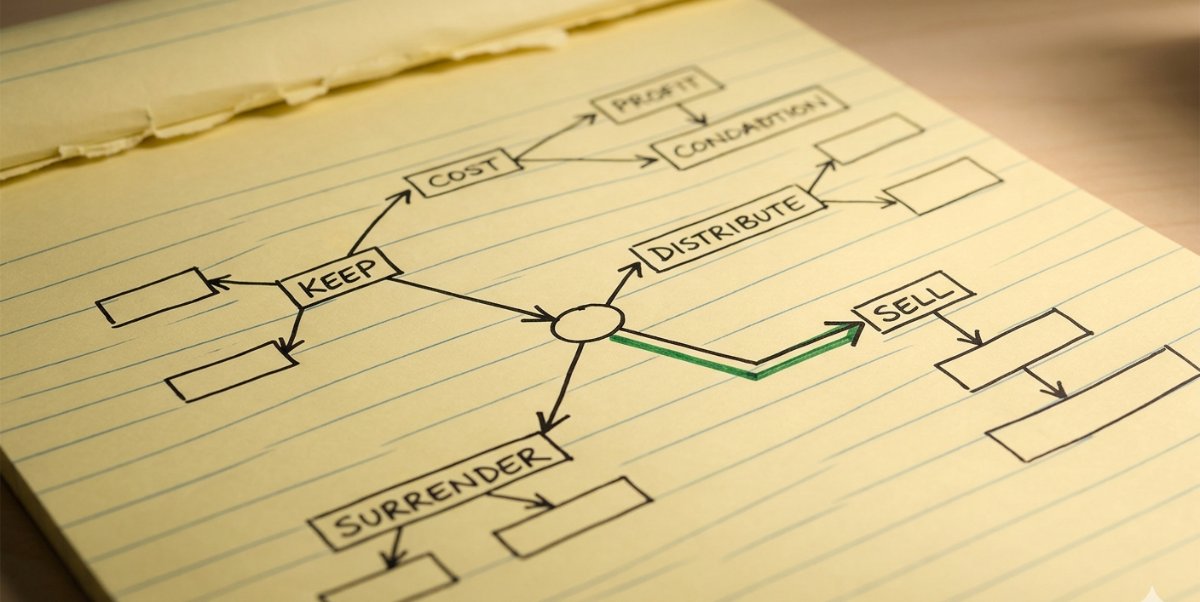

The four options: keep, distribute, sell, surrender

When the planning purpose has shifted

, the trustee’s practical universe of options narrows to four.

Keep. The premiums continue to be paid, either from trust assets, from Crummey contributions by the grantor, or from a combination. The policy remains in force; the death benefit eventually flows to the trust as originally contemplated. This is the right answer when the original liquidity or equalization purpose remains valid and the premium burden is sustainable.

Distribute. The trustee distributes the policy in-kind to one or more beneficiaries. The trust ends or continues with reduced corpus. The beneficiary owns the policy and is responsible for premiums. The trustee must consider whether the trust instrument permits the distribution, the tax consequences to the beneficiary, and any transfer-for-value implications.

Sell. The trustee enters into a life settlement, conveying the policy to a third-party buyer at the market price. Trust receives cash proceeds, which are then administered according to the trust terms. The transfer-for-value rule must be analyzed; in most arm’s-length settlements to an unrelated buyer, the rule applies to the buyer’s position but does not eliminate the trust’s tax-free recovery of basis under standard life-settlement rules.

Surrender. The trustee surrenders the policy to the carrier for cash value. Generally the lowest-yield option. Used when no third-party market exists for the policy (often the case for term contracts or smaller policies where transaction cost outweighs settlement premium).

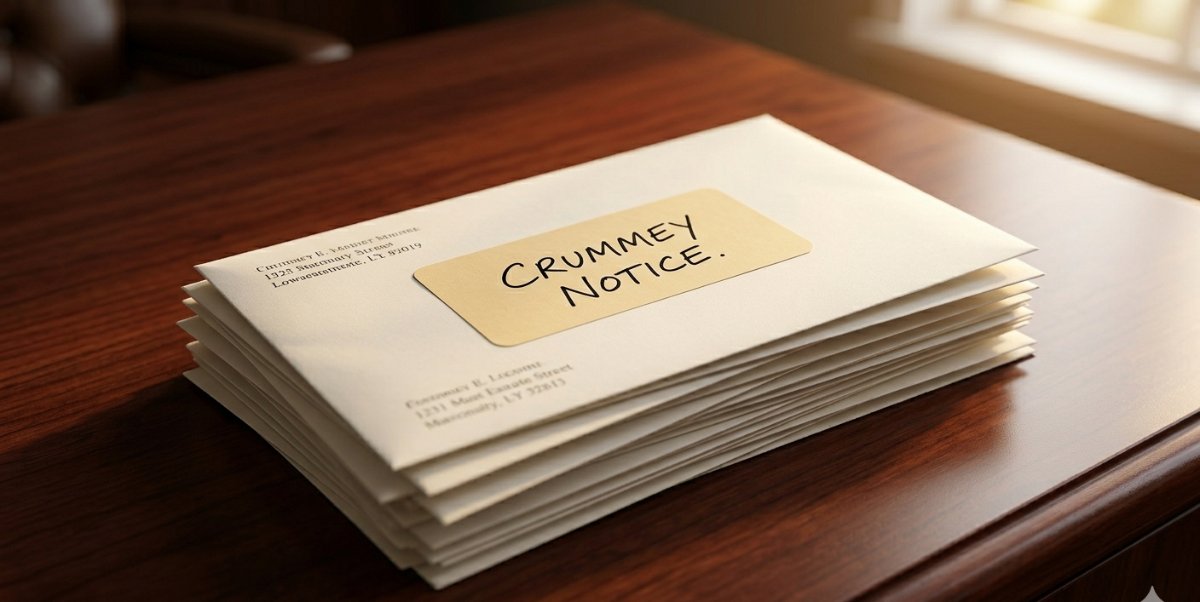

Crummey powers and contributions

Most ILITs are funded by annual Crummey-power contributions from the grantor, which provide beneficiaries with a brief window of withdrawal right after each contribution. The mechanism is designed to qualify the contribution for the federal gift-tax annual exclusion under §2503(b). Each contribution requires a Crummey notice to each holder of a withdrawal right.

When the policy reaches a decision point, the question for the trustee is whether continued Crummey contributions remain advisable. If the policy is to be retained, the contribution stream must continue. If the policy is to be sold or distributed, the next contribution cycle may be the opportunity to wind down the funding mechanism in a coordinated way — preserving the year’s exclusion benefit if useful, or stopping contributions cleanly if not.

Practitioners should also confirm that the trust’s Crummey procedures have been observed without gaps in prior years. Defective Crummey notices in the file can complicate the eventual gift-tax-return position and may surface during the trust’s administration of the settlement proceeds.

The transfer-for-value rule

Internal Revenue Code §101(a)(2) — the transfer-for-value rule — provides that life insurance death benefits paid to a transferee who acquired the policy for valuable consideration are taxable to the transferee, except in a limited set of safe harbors. The rule does not affect the seller’s tax position; it affects what the buyer will eventually receive.

For ILIT-held policies sold into the secondary market, the transfer-for-value rule applies to the buyer. The buyer, knowing this, prices accordingly. From the trustee’s perspective, the rule is largely a buyer-side issue — but practitioners should be aware of it because it is the reason settlement prices are calibrated to the buyer’s expected after-tax position.

If the policy is distributed in-kind to a beneficiary who is also the insured’s family member, transfer-for-value concerns may not arise because the safe harbors (transfer to the insured, to a partner of the insured, or to a partnership in which the insured is a partner) may apply or the distribution may not constitute a transfer for valuable consideration in the first place. The analysis is fact-specific.

Beneficiary consent and notice

Whether a trustee must obtain beneficiary consent before a settlement depends on the trust instrument and the relevant state trust code. Most modern trust instruments grant the trustee broad authority over trust property, including the right to sell trust assets. Beneficiary consent is generally not required as a matter of governing law, but it is often advisable as a matter of practice. A clear record of beneficiary acknowledgment can foreclose later claims that the disposition was imprudent.

State trust statutes also typically provide for a trustee’s ability to request a virtual representation of unascertained or minor beneficiaries, or to obtain a court order approving the proposed transaction. In larger or more complex trusts, a court order can be the prudent path; in smaller trusts, a written beneficiary acknowledgment is generally sufficient.

Documenting the trustee’s decision

The trustee’s file should reflect:

The annual policy review. A short memo each year documenting the in-force value, the cash surrender value, the current premium outlay, and any change in the grantor’s circumstances or estate plan that would affect the original purpose.

Quotes and offers. If a settlement is considered, offers from multiple licensed providers create the market evidence supporting the eventual disposition price.

Counsel opinion on transfer-for-value, distribution, or sale. A brief opinion letter from trust counsel addressing the proposed disposition and any tax or fiduciary considerations.

Beneficiary acknowledgment. Written acknowledgment from the beneficiaries (or virtual representatives) of the proposed disposition, even where not legally required.

Closing documentation. Standard closing package — the licensed provider’s disclosures, the bill of sale, the §6050Y Form 1099-LS, and the carrier’s confirmation of ownership transfer.

Tax character of the proceeds

Settlement proceeds received by the trust are subject to the three-tier framework like any other settlement. The trust’s tax character — grantor, non-grantor, complex — determines who realizes which slice.

For a grantor trust, the grantor is the income tax owner and reports accordingly on the grantor’s personal return. For a non-grantor trust, the trust reports the income on its own fiduciary return, with distributable net income concepts then applying to flow income through to beneficiaries to the extent the trust distributes corpus. The interaction with Crummey-power mechanics, the trust instrument’s distribution provisions, and any tax-allocation language in the trust will shape the final allocation.

For detailed treatment of the three-tier framework and the §6050Y reporting obligations that follow the proceeds, see the companion guide on life settlement tax treatment.

Practice points

Treat the annual review as a fiduciary obligation, not a courtesy. Beneficiary claims for breach of fiduciary duty in the ILIT context often trace to years of passive trustee behavior. The annual review memo is the trustee’s best defense.

Get multiple offers before a settlement. Beyond the practical pricing benefit, multiple offers establish market evidence of fair value, which protects the trustee and supports the eventual tax position.

Coordinate with the grantor’s estate plan. The ILIT was created in service of a broader estate plan. Any disposition should be reconciled with the current plan, particularly if the grantor remains alive and competent.

Mind the Crummey paperwork. Defective notices undermine annual exclusion treatment. Confirm clean files for the years contribution-supported the policy, and document the closure of the contribution stream when the policy is sold or distributed.

Cross-check Medicaid implications where applicable. If the grantor is a long-term-care candidate, the trust’s funding pattern and the timing of any disposition may matter. See the companion guide on Medicaid spend-down and life insurance.

Frequently asked questions

Does selling a policy from an ILIT require court approval?

Generally no, where the trust instrument grants the trustee broad authority over trust property and the relevant state trust code permits sale. For larger trusts or where ambiguity exists, a court order is the prudent path. Most practitioners proceed on written beneficiary acknowledgment in smaller cases.

Does the transfer-for-value rule reduce the proceeds the trust receives?

The rule affects the buyer’s tax position on the eventual death benefit, not the seller’s tax position. It is reflected in the price the buyer is willing to pay. Practically, settlement pricing already accounts for it.

Can the trustee distribute the policy in-kind to a beneficiary?

If the trust instrument permits, yes. The beneficiary takes the policy subject to its terms and assumes the premium obligation. Tax and transfer-for-value implications should be analyzed before distribution.

What happens to the Crummey-power mechanism after the policy is sold?

If no further contributions are needed (because the trust now holds cash from the settlement rather than a policy requiring premium support), the Crummey-power mechanism may simply go dormant. Practitioners should document the wind-down for the file and ensure no inadvertent contributions are made after the disposition.

How are the proceeds taxed inside the trust?

The three-tier framework applies. For a grantor trust, the grantor is the income tax owner and reports accordingly. For a non-grantor trust, the trust reports the income, with distributable net income rules then governing flow-through to beneficiaries.

What if the policy was placed in the ILIT decades ago and the original lawyer’s file is gone?

The trustee should reconstruct the file from the carrier’s records, available historical tax returns, and any surviving correspondence. The carrier’s premium history and the trust’s historical tax returns will generally establish basis and Crummey-contribution patterns. A reconstructed file is materially better than no file.

Primary sources cited

- Uniform Prudent Investor Act (state-enacted versions)

- Internal Revenue Code §2503(b) — gift-tax annual exclusion

- Internal Revenue Code §101(a)(2) — transfer-for-value rule

- Crummey v. Commissioner, 397 F.2d 82 (9th Cir. 1968)

- Internal Revenue Service Revenue Ruling 2009-13

- Internal Revenue Service Revenue Ruling 2009-14

- Internal Revenue Code §6050Y — reportable policy sale reporting

- National Association of Insurance Commissioners (NAIC) Model #697 — Viatical Settlements Model Act

For a confidential review of a specific ILIT-held policy and the settlement-vs-distribute-vs-surrender analysis, call Pine Lake at (305) 209-7183 or visit the Contact page. Pine Lake’s free For Professionals library includes the 50-state regulatory map and Verify-a-Broker DOI lookup tool.

Important Notice

Pine Lake Life Solutions provides educational information only. The content of this article is general in nature and does not constitute legal, tax, or financial advice for any specific situation. Life settlement transactions are regulated at the state level and the rules vary materially across jurisdictions. Pine Lake Life Solutions facilitates life settlements and is compensated when transactions close — a material conflict that practitioners should weigh when relying on this content. Always verify statutes, IRS guidance, and NAIC model provisions directly with primary sources, and confer with independent legal, tax, and fiduciary counsel before advising a client. To discuss a specific case confidentially, call (305) 209-7183 or visit our Contact page.